Since January 2019, the P2P Portfolio Update has been a regular feature on my blog. Each month, investors receive a transparent overview of the developments in my personal P2P lending portfolio, including income, performance, transactions, and portfolio value.

Additionally, I cover potential changes or adjustments at the P2P Platforms included in my portfolio. Detailed platform analyses can be found on the P2P Platform Reviews page.

For up-to-date information, I recommend following my Telegram or WhatsApp channels, where timely reactions, evaluations, and insights are shared as soon as new developments occur.

P2P Portfolio Update: March 2026

Here is the current state of my personal P2P lending portfolio as of the end of February 2026.

Income

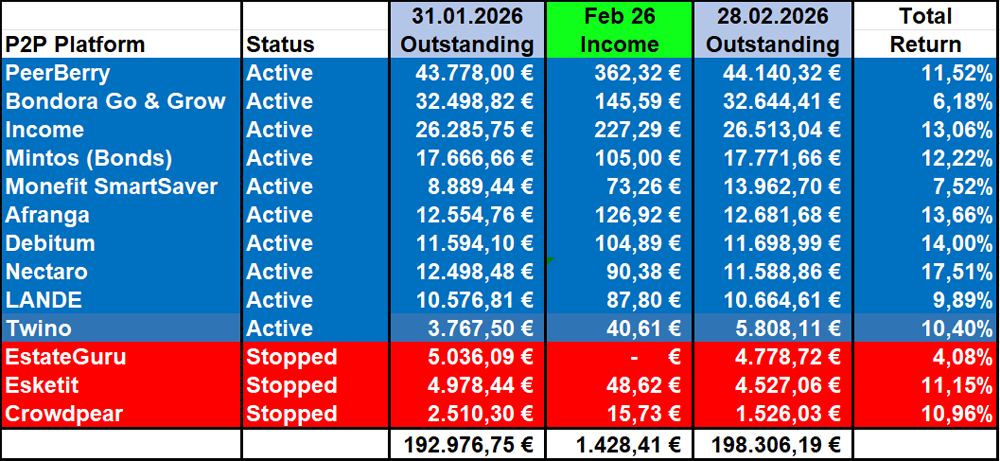

In February 2026, I earned EUR 1,428 in income from my outstanding P2P lending portfolio. Despite the continued growth in portfolio value, this represents only the fifth-highest monthly income I have achieved in the past eight and a half years with my P2P portfolio.

Performance

The best overall performance in my P2P portfolio currently comes from Nectaro at 17.5%. The above-average return is driven by my active investment approach, which is aligned with the platform’s various bonus campaigns. In second place comes Debitum at a solid 14%, followed by Afranga at 13.7% and Income Marketplace at 13.1%.

Transactions

Last month, there were a total of five new transactions in my P2P portfolio.

Deposits: EUR 7,000

- Monefit SmartSaver: EUR 5,000. The funds went only into the main account, which earns 7.5% APY, to maximize liquidity.

- Twino: EUR 2,000. My position on Twino continues to grow. The new funds were invested in Polish Asset-Backed Securities with a 12-month term and 12% interest.

Withdrawals: EUR 2,500

- Nectaro: EUR 1,000. Available funds were withdrawn until the next bonus campaign. Regardless, I plan to reactivate the portfolio once it reaches approximately EUR 8,000.

- Crowdpear: EUR 1,000. Multiple repayments occurred last month, allowing for this withdrawal in February.

- Esketit: EUR 500. Similar situation at Esketit. For the time being, repayments from the “Ireland Portfolio” are being withdrawn.

Overall, the net deposit/withdrawal ratio last month was EUR 4,500.

P2P Portfolio

The value of my outstanding P2P lending portfolio increased from EUR 192,977 to EUR 198,306 in February 2026. The liquidity-focused portion of my portfolio, consisting of Bondora Go & Grow and Monefit SmartSaver, amounted to EUR 46,337, representing 23.4% of the total portfolio.

P2P Lending Update: March 2026

Next up, a summary of the most important events and developments that have recently happened in the P2P lending industry. Details on loan originator developments can be found on my lender overview and comparison page.

PeerBerry with New Secondary Market Rules

PeerBerry has reactivated its temporarily paused secondary market and implemented several new rules. For example, all loans can now only be sold at the base interest rate. The additional interest bonus for investors in the loyalty program is therefore no longer applied when selling.

A significant limitation affects investors by loans to be only sold on the secondary market after a holding period of 180 days. The same period also applies to buyers purchasing investments through the secondary market.

Despite these rather investor-unfriendly restrictions, PeerBerry continues to find buyers for their now slightly increasing loan supply. By the end of February, the managed portfolio reached a new record value of EUR 118.2 million.

Income Marketplace Working on Secondary Market Launch

Income Marketplace has grown its outstanding portfolio to over EUR 26 million. The default rate, impacted by the Clickcash default (with EUR 88,000 still outstanding), is now at an impressive 0.33%. CEO Lavrenti Tsudakov stated that, due to the prioritization of secondary market development (“we expect to move into testing soon”), the Estonian marketplace did not make any bridging payments in February.

Mintos Raises EUR 2.8 Million; Launches “Investment Plan” Feature

In its latest funding round, Mintos raised approximately EUR 2.8 million from nearly 6,000 investors. The company plans to use the funds to apply for a banking license with the European Central Bank (ECB) within the next 12–18 months. If successful, Mintos could offer bank products with deposit protection in the future and further expand its product offerings.

Additionally, Mintos introduced a new feature called Investment Plans, which allows investors to set up recurring transfers for automated portfolios (Core Loans, Custom Loans, High-Yield Bonds Portfolio, and ETF Portfolio). Available frequencies include weekly, biweekly, monthly, or quarterly.

To set up an Investment Plan, investors simply select “Investment Plan” in the automated portfolio, choose the date, frequency, and the transferred amount. Each automated portfolio now has its own cash wallet, meaning funds are no longer deducted from the overall account balance. As a result, the “Keep Available” function for Core Loans and Custom Loans has been removed.

Afranga Launches “SaveSmart”; 16% Stikcredit Loans

Afranga has introduced “SaveSmart”, a new fixed-interest investment product. Depending on the chosen term, investors can earn returns of 8% (3 months), 10% (6 months), or 12% (12 months). Interest is paid monthly, while the principal is returned at the end of the term. An early exit option or the sale of the investment is not possible.

Currently, investments via SaveSmart are made as private loans to the Bulgarian lender Stikcredit, though additional lenders may be added in the future. For investors focused more on yield than liquidity, it is still possible until March 31, 2026, to invest in Stikcredit loans with 16% interest and a 36-month term.

Debitum Lender LFDF Reports EUR 1.6 Million Profit in 2025

The Latvian Forest Development Fund (LFDF), currently the largest lender on Debitum, has published its unaudited financial figures for 2025. According to these, EUR 33.2 million were invested in the acquisition of 659 forest plots, covering an area of 6,430 hectares. An operating net profit of EUR 1.6 million was achieved, while the equity position roughly doubled to around EUR 3 million.

TWINO Repays over EUR 1 Million in Russian Loans; Deep Dive Analysis

In February, TWINO offered its investors the option to transfer the outstanding claims of Russian loans to the parent company SIA FINNO at a 20% discount. For this, a cash position of EUR 200,000 was made available.

In the current interview with the TWINO CEO, however, he mentioned that demand was four to five times higher than expected.

As can be seen from the latest portfolio update, TWINO recently repaid approximately EUR 1.13 million of Russian claims. For the remaining EUR 800,000 in outstanding claims, a repayment period is now expected to extend until the end of 2026. Under the leadership of CEO Nauris Bloks, TWINO has thus successfully resolved the platform’s next major issue.

In my current deep dive analysis of TWINO, I explore the specific changes since the CEO transition in April 2025, where the platform is heading in 2026, and whether an investment is now worthwhile again.

Estateguru with Update on Recoveries in 2025

Estateguru published an article providing new insights regarding recoveries in its various markets. According to the article, the platform has historically recovered EUR 63 million in defaulted loans. Of this amount, EUR 14.8 million relate to 2024 and EUR 7.5 million to 2025.

On the other hand, a monthly cost of EUR 100,000 to EUR 150,000 (EUR 1.7 million in 2025) is incurred for managing the defaulted loans. This includes fees for lawyers and brokers, bailiff costs, as well as expenses for insurance, insolvency management, and collateral protection.

Considering the financial effort Estateguru expends on recoveries, the results can be described as rather disappointing. With nearly EUR 120 million in defaulted loans and a default ratio of more than 60%, Estateguru still has the worst portfolio quality of all active platforms in the entire P2P market.

Esketit Buys Back 30% of Outstanding Ireland Loans

In November 2025, Esketit announced that it would repurchase up to 30% of the outstanding Esketit Ireland loans by the end of March 2026. According to the P2P platform, this process was successfully completed on February 27, 2026. Approximately EUR 12.9 million were thus repaid early to 8,102 affected investors.

However, this is not the end of the process, as Esketit plans to redeem additional loans from the Ireland portfolio early by the end of the year. Specifically, the platform plans to buy back another EUR 21.7 million by the end of 2026. This would bring total repayments to EUR 34.6 million, representing nearly 80% of the original Ireland portfolio.

New Lender on Lendermarket; All Fees Removed

The Colombian lender RapiCredit is expanding its business model to Spain. The consumer loans are being offered on Lendermarket with interest rates of up to 15% and terms ranging from 30 to 180 days. The standard buyback guarantee will also apply. Since the lender was only founded in November 2025, no financial statements are currently available to assess its stability.

At the same time, Lendermarket announced that, as of March 9, 2026, all platform fees will be waived. Previously, there was a EUR 2 withdrawal fee (from the second withdrawal per calendar month) as well as a 1.95% transaction fee for card deposits and withdrawals.

Martin Stibor Becomes the New Bondster CEO

The Czech P2P marketplace Bondster has appointed Martin Stibor as its new CEO. He brings many years of experience in investment management and strategic financial planning. Prior to joining Bondster, he spent six years at CEP Invest, where he was responsible for evaluating both publicly listed and private investment opportunities, as well as coordinating investment processes.

Swaper Appoints New CEO

The Estonian P2P platform Swaper has appointed Aigars Boruks as its new CEO. He succeeds Indrek Puolokainen, who had held the position since 2020. Aigars brings more than 16 years of professional experience in fintech, banking, and auditing. In recent years, he has also advised P2P platforms on corporate governance and business development.

Looking ahead, he plans to expand the network of loan originators on Swaper. At the same time, the platform is expected to be further improved through enhanced functionality, automation, and more advanced portfolio tools.

I’m Denny Neidhardt, the founder of re:think P2P. On this blog, I help retail investors make smarter, well-informed investment decisions in the world of P2P lending. Since 2019, I’ve been publishing in-depth analyses, platform reviews, and risk assessments to bring more transparency to this investment space. My goal is to challenge marketing claims, question developments, and empower investors with honest, independent insights.