With established loan originators, reliable repayments, high liquidity, and competitive interest rates, Esketit had developed since late 2020 into one of the most attractive platforms in the P2P lending space. In 2023, Esketit was even voted the most popular platform in the annual P2P community voting.

After years of steady development, 2025 has brought a change to Esketit: established loan originators have left the platform, the operational management changed, and the jurisdiction was changed to Croatia, resulting in significant liquidity constraints for investors.

In this Esketit review, all investment-related criteria are being discussed, including the various risks that investors should be aware of. Is it worth investing on Esketit in 2026? Let’s find out!

Further analyses of other platforms can be found on my P2P Platform Review page.

Summary

Before we get started, here is a quick summary with the most important information about Esketit.

- Esketit is a Croatia-registered P2P platform where investors can invest in business loans and consumer loans. Expected returns are often in the low double-digit range.

- Esketit was primarily established as a financing platform for the international lending activities of its two Latvian shareholders, who have decades of experience in the non-bank lending sector.

- Thanks to the combination of competitive interest rates from profitable loan originators, high liquidity, and reliable repayments, Esketit has been one of the fastest-growing P2P platforms in Europe since its founding in 2020.

- The platform’s popularity is supported by excellent results in the annual community voting. In 2023, Esketit ranked first out of 30 P2P platforms, and in 2024 it finished in fifth place.

- Due to the exit of established loan originators (AvaFin), the relocation to Croatia (which led to liquidity constraints for investors), and insufficient communication from the platform, Esketit lost attractiveness in 2025.

| Founded / Started: | July 2020 / December 2020 |

| Legal Name: | Esketit Platform d.o.o. |

| Headquarter: | Zagreb, Croatia |

| Regulated: | No |

| CEO: | Ieva Grigaļūne (July 2025) |

| Community Voting: | P7 out of 30 | See Voting |

| Assets Under Management: | EUR 46+ Million |

| Number of Investors: | 29.000+ |

| Expected Return: | 11.83% |

| Primary Loan Type: | Consumer Loans |

| Collateral: | Buyback Guarantee |

| Bonus: | 0.5% Cashback for 90 Days |

What is Esketit?

Esketit is a Croatia-based P2P platform that launched in December 2020. On the platform, investors can invest in both consumer loans and business loans. The offered interest rates are often in the high single digit or low double digit range.

Esketit was founded by two experienced entrepreneurs, Matiss Ansviesulis and Davis Barons, who have been active in the international non-bank lending sector since 2012. Through Esketit, the founders created a financing platform to support the lending activities of the loan originators they established.

Thanks to the combination of competitive interest rates from profitable loan originators, high liquidity, and reliable repayments, Esketit has been one of the fastest-growing P2P platforms in Europe since its founding in 2020.

Interestingly, the name “Esketit” is based on a song and a frequently used word by the US rapper Lil Pump, who came up with the expression “esketit” which refers to “Let’s get it”.

The Origin Story

Esketit was founded in July 2020. The launch of the website happened in December 2020 and the first loans have been issued in March 2021.

Esketit was founded in July 2020. The launch of the website happened in December 2020 and the first loans have been issued in March 2021.

The driving forces behind Esketit are the two founders Matiss Ansviesulis (left) and Davis Barons (right), who have already built a succesful company with AvaFin Holidng, formerly known as Creamfinance.

The idea behind Esketit is to establish a low-cost funding source for their worldwide lending operations.

Ownership and Management

Who are the main shareholders and management executives behind Esketit? Let’s have a look!

Esketit Ownership

Who owns Esketit? A look into the Irish company register reveals that “Esketit Platform Ltd.” is owned 50% each by the two founders Davis Barons and Matiss Ansviesulis.

Both shareholders had already founded the Latvia-based SIA Cream Finance in 2012. This company was an internationally operating non-bank lender in the private consumer loan segment. Here too, the shares were split equally, with each Latvian founder holding 50%.

Back in 2019, I was able to meet Matiss Ansviesulis in Riga, one of the Esketit owners. At the time, we also recorded a short interview during our meeting. In 2024, as part of my travels through the Baltics, I was able to meet both Esketit shareholders on-site in Riga and discuss a few topics.

Esketit Management

On July 30, 2025, Latvian Ieva Grigaļūne has been appointed as the new CEO of Esketit. She succeeded Vitālijs Zalovs, who has been with the platform since the beginning in 2021.

Ieva brings nearly 10 years of professional experience working for Mintos, where she was responsible for business development, risk management, and product management.

As a result, Esketit is now led by an experienced and industry-savvy manager. Her main responsibilities include overseeing the operational structure, continuing the platform’s expansion, and implementing licensing.

Business Model and Finances

Throughout the due diligence process, investors should also have a look at the business model of a P2P platform as well as the overall financial situation. How does the company earn money? Does the platform operate profitably? And how well is the company positioned financially? Find out more about those topics in the following paragraphs of this Esketit review.

Monetization

How does Esketit earn money? The platform generates its revenue primarily through commission fees charged to the lenders represented on the marketplace. These are divided into a fixed fee and a variable fee. The flexible fee depends on the financed loan volume on the platform.

The average commission is around 2%, which corresponds to a standard market percentage.

Profitability

Is Esketit profitable? According to the platform, profitability was achieved on a monthly basis in the second half of 2022. The threshold for this was an outstanding loan portfolio of around EUR 20 million. This enabled the platform to cover its total expenditure of around EUR 33,000 per month.

However, there are no reliable figures for this, as Esketit has not yet published audited annual financial statements.

On the flip side, profitability plays a subordinate role at Esketit for two reasons:

- Esketit’s aim is not to be profitable, but to finance the lending operations of both shareholders.

- As both owners are multi-millionaires, they can guarantee the maintenance of the platform at all times.

Even if Esketit were not profitable, investors should take these two factors into account. Regardless of this, however, it would be desirable for the platform to provide insights into its financial performance.

Sign Up and Bonus

To invest on Esketit, investors must meet two requirements: A minimum age of 18 years and a bank account in the European Union or the European Economic Area.

The sign-up process on Esketit is fairly simple and intuitive. After opening the account via email, the KYC and AML questionnaires must be completed. After that, the verification of the identity takes place as well as from the bank account.

Also legal entities have the opportunity to register with Esketit.

Esketit Bonus

If you consider investing on Esketit, a sign up through this link will enable you to get an unlimited cashback bonus of 0.5% for the first 90 days after registration. A platform overview with all bonus offers and cashback promotions can be found on the bonus page.

Investing on Esketit

How does Esketit work and what should investors know and consider when investing on the plaform? In the following sections of this Esketit review you will find all the necessary information that you need.

Loan Offering

On the Esketit marketplace, there are a variety of international lenders financing their loan portfolios through the P2P platform. Here’s a brief overview:

- Spanda Capital: A Latvia-based company founded by the two Esketit shareholders. Specializes in acquiring non-performing consumer loan portfolios (NPLs) in Spain. Present on Esketit since January 2024. Offers interest rates of up to 11%.

- Mojo Capital: A globally operating lending company based in the United Arab Emirates, also owned by the two Esketit founders. Specializes in financial services and products specifically targeted at fintech companies and asset management. Business loans are offered at 12% interest with a two-year term.

- MDI Finance: Since August 2025, business loans from MDI Finance can be financed. The Latvia-based holding company is supporting the lending business of the Sri Lankan lender loanme.lk. The holding is owned by the two Esketit founders. Loans are offered at up to 12% interest.

- A24 Group: A non-bank lender established 2010 in Latvia. Offers secured mortgage loans with interest rates of 7%.

- Credus Capital: Part of the A24 Group, created specifically for cooperation with Esketit. Provides an additional layer of security as Esketit holds a lien over the entire business. Offers mortgage loans with solid collateral (LTV < 70%) and terms of up to three years.

Costs and Fees

For investors, there are no costs or hidden fees on Esketit. This applies to account maintenance, deposits, withdrawals, or any other services. Unfortunately, this is no longer a given on many other P2P lending platforms.

Expected Returns

The interest rates on Esketit are determined by the lenders and thus can be adjusted flexibly. At the moment, the range for interest rates on Esketit is currently between 7% and 12%.

Personally, I have been continuously investing on Esketit since October 2022. During this time, I have achieved a total return of 11.15%, which corresponds to a realistic return expectation.

If you invest enough money on the platform, you can improve your return even further. With an outstanding portfolio of more than EUR 25,000, you will receive an additional 0.5% interest and with more than EUR 50,000 even 1% more interest on all loans.

Auto Invest

On Esketit, investors can invest in loans either manually or via the Auto Invest feature. This allows loan repayments to be automatically reinvested according to the criteria chosen in advance. The Esketit Auto Invest is further divided into two types: the “Esketit Strategies” and the “Custom Strategies.”

Custom Strategies are more or less the classic Auto Invest. Investors can select individual lenders, borrower countries, the term of the loans, the interest rates, the investment amount, the loan type as well as the buyback guarantee option.

For the Esketit Strategies, there is currently only one predefined investment option. The “Diversified” strategy automatically invests in all available loans. The allocation is evenly divided, with 20% each in Spanda Capital, Mojo Capital, JMD Investments, Mortgage Loans, and MDI Finance.

Investors who choose one of the predefined Esketit strategies can, if needed and depending on market demand, liquidate their entire loan portfolio immediately using the Cashout function.

Secondary Market

Esketit offers a secondary market where investors can both buy and sell loans early. When selling, a premium (up to 2%) or a discount (up to 20%) can be applied. There are no costs or fees for using the secondary market.

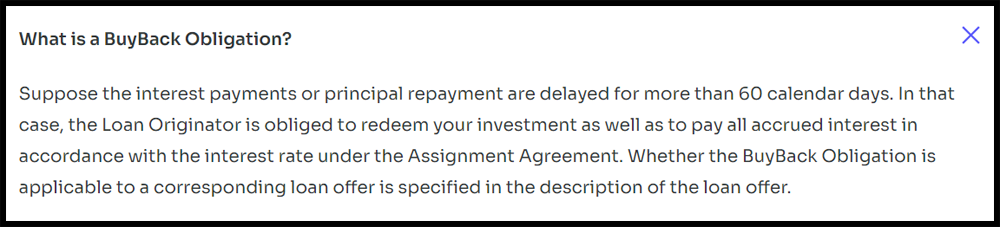

Buyback Guarantee

Esketit promotes the concept of a buyback guarantee, whereby the loans are repurchased by the lenders after the loans are 60+ days late in the repayment schedule. Here, also the accrued interest is reimbursed.

So far, the buyback guarantee on Esketit has always been honored by all lenders.

Esketit Forum

The P2P lending industry is a fast-moving environment. Hence, make sure to stay on top of all relevant information by subscribing to my channels on Telegram or WhatsApp. This way, you will always receive the latest information from the P2P industry, including platform news regarding Esketit.

Esketit Taxes

Generally, interest income generated by loan financing is considered investment income and must be reported as such on the tax declaration. Unlike other platforms, Esketit does not withhold any taxes at the moment.

For the tax declaration, investors can download an income statement for tax report purposes as PDF within the “Statement” tab in the main menu. This information can then be used and forwarded to the tax office.

Esketit Risks

When considering a P2P platform, investors should take a very close look at the potential risk factors and evaluate them before making an investment. What should be considered in the specific case of Esketit? What are the underlying risks and how can they be assessed?

Platform Risk

Esketit was founded in December 2020, with operations officially starting in March 2021. The platform is registered in Ireland as “Esketit Platform Limited.” Consequently, the company is not subject to any form of licensing by a regulatory authority or financial supervision. This enables Esketit to operate with a reduced amount of legal requirements, which in turn is limiting investors protection in terms of transparency and compliance. For example, the platform hasn’t published any audited financial statements of the platform to date.

Therefore, it is important to check whether the platform’s shareholders can be trusted.

On the positive side, it should be noted that both Esketit shareholders have an excellent reputation, are already financially secure, and have successfully established many profitable business models in different borrower countries in the past.

In addition, Esketit was primarily set up as an interface to finance the shareholders’ new fintech ventures, with profitability playing a rather secondary role. Considering the shareholders’ situation as outlined, the platform risk can be regarded as relatively minor.

Nevertheless, trust-building measures such as the licensing of the P2P platform, publishing audited financial reports, and placing a stronger focus on communication with investors would certainly be desirable.

Deposit Insurance

What happens if Esketit were to go bankrupt or file for insolvency for any reason? In this case, investors should note that the investments offered through Esketit are not covered by European deposit insurance schemes. This means that—unlike traditional bank deposits—the funds invested on Esketit are not insured or guaranteed by any national or European compensation system.

Investors should therefore be aware that the invested capital is exposed to a real risk of loss, returns are not guaranteed, and it is possible that the full invested amount may not be recovered.

However, the claims against the lending companies remain valid and can still be enforced legally.

Lender Risk

The founders of Esketit have over 10 years of experience in the international lending business. It is therefore reasonable to assume that they understand what to look for, both with their own lending companies and with external lenders.

If individual loan defaults occur, they are covered by the lenders’ buyback guarantee. To date, this guarantee has been honored by all lenders without exception.

It is also worth noting that all lenders on the marketplace are regulated and thus subject to national rules and regulations for lending. Should a lender nonetheless encounter problems, investors still retain claims and rights against the borrower.

However, a comprehensive analysis of each lender is difficult for investors, as many loan originators have only a limited track record and therefore provide few or rarely meaningful figures on business performance.

| Loan Originator | Year | Audited | Profit | ROA | Equity Ratio | Debt | Liquidity | Impairments | Score |

|---|---|---|---|---|---|---|---|---|---|

| A24 Group | |||||||||

| Credus Capital | |||||||||

| Jet Finance | 2024 | Grant Thornton | EUR 1,18M | 4,3% | 20,6% | 3,86% | 14,9 | 7,6% | 77 |

| JMD Investments | 2024 | Baker Tilly | EUR 4,63M | 32,2% | 51,8% | 0,93% | 0,25 | 60 | |

| MDI Finance | |||||||||

| Mojo Capital | 2024 | Unaudited | (USD 98K) | (5,7%) | (18%) | 2,83 | 32 | ||

| Spanda Capital | 2024 | Cortés y Asociados Auditores | EUR 12K | 0,4% | 0,2% | 447 | 1,74 | 35 |

Check out the lender overview and comparison page for additional information regarding applied KPIs and their interpretation.

Advantages and Disadvantages

In this section, I have listed the most important advantages and disadvantages of Esketit.

Advantages

- Shareholders: Many years of experience in the lending business.

- Diversification: Wide range of international loan originators.

- Liquidity: Short-term assets, secondary market, and early cash-out option.

- Reliability: Delayed loans are regularly bought back.

- Losses: No investor losses to date.

- Fees: No costs or hidden fees on the P2P platform.

- Auto Invest: Passive income with P2P loans thanks to automated investment options.

Disadvantages

- Regulation: The platform is not overseen by any regulatory authority or financial supervisor.

- Experience: Many new and young fintech companies with limited track record.

- Liability: Investors may potentially bear part of the costs of a recovery process.

- Conflicts of Interest: Overlapping shareholder interests between the platform and many of the loan originators.

Esketit Alternatives

Esketit’s business model is best compared with other P2P marketplaces. Therefore, the most similar Esketit alternatives can be found on platforms such as Income Marketplace, Mintos or Debitum Investments.

Income Marketplace

Income Marketplace is an unregulated P2P marketplace based in Estonia. The platform, which had its operational start in January 2021, markets itself with a range of innovative security features that are designed to provide investors with significantly better protection against problematic lenders. So far, investors have not suffered any losses on Income Marketplace yet. In addition, many of the lenders represented on Income offer an attractive combination of high interest rates and high liquidity. Further information on the Esketit alternative can be found in my Income Marketplace review.

Mintos

With EUR 600+ million in investor assets under management and more than 500,000 registered users, Mintos is the largest P2P lending platform in Europe. In addition to a wide range of loans, the Latvian P2P marketplace also offers other asset classes. These include ETFs, bonds or real estate. Additional information can be found in my Mintos review.

Debitum Investments

Debitum Investments (formerly Debitum Network) is a P2P marketplace based in Latvia and regulated by the local financial supervisory authority. What makes Debitum special is its unique positioning in the P2P lending environment, as it is regulated, follows a marketplace model and offers buyback-secured business loans. A combination that cannot be found in this particular form on any other P2P platform. Additional information can be found in my Debitum review.

You can find other Esketit alternatives on the P2P Platform Comparison page.

Esketit Community Feedback

Community experiences with Esketit are extremely positive. At least if the results of the annual P2P Community Voting are taken as a benchmark. Over the past three years, Esketit has consistently ranked among the seven best and most popular P2P lending platforms. In 2023, it was even rated as the number one P2P platform.

The Top 5 P2P platforms in 2025 were Viainvest, Debitum, Mintos, Swaper, and Income Marketplace.

Summary Esketit Review

What the final verdict of my Esketit review and which conclusions can be drawn for investors?

What the final verdict of my Esketit review and which conclusions can be drawn for investors?

Esketit is an Ireland-registered P2P platform where investors primarily invest in business loans from internationally operating lenders, earning returns of up to 12%.

The popularity of Esketit, which has led to two top 5 rankings in the 2023 and 2024 community voting, is relatively easy to explain: The platform offers competitive interest rates, coupled with high liquidity and reliable repayments. Achieving a double-digit return with Esketit is therefore absolutely realistic.

What also speaks in favor of Esketit is the experienced founder duo, who have built and established profitable business models in a wide range of borrower countries for more than a decade. Esketit is therefore set to establish itself as one of the best options in the P2P lending space for the long term.

However, the change that Esketit has been undergoing since 2025 should also be taken into account: established lenders like AvaFin and Money for Finance have exited the platform, the operational management has been replaced, and there are increasing indications of a planned licensing.

The departure of some bigger lenders is particularly significant, as Esketit is now increasingly taking on the profile of a P2P marketplace for new fintech startups with only a limited track record. The absence of financial figures therefore makes an objective evaluation of these companies difficult.

Nevertheless, for those who believe in the success story of the P2P platform and value the founders’ previous performance and know-how, Esketit represents a reliable alternative for your P2P portfolio.

FAQ Esketit Review

Esketit is a P2P lending marketplace incorporated in Croatia. The platform primarily provides funding to fintech companies owned by its two shareholders to support their business development. Following its operational launch in December 2020, Esketit was, for many years, one of the most popular and fastest-growing platforms in the market.

On Esketit, interest rates vary depending on the market phase and the loan originator. The range is typically between 7% and 12%. An expected return in the low double digits can be considered realistic. Since 2022, the re:think P2P lending portfolio has achieved an average annual return of 11.15%.

In my Esketit review, the platform’s risks have been described in detail. It should be noted that Esketit is not supervised by any financial authority (lack of regulation), there is no deposit protection, and loan originator risk has a significant impact on the returns that can be achieved.

Yes, Esketit offers a buyback guarantee. This means that loans must be repurchased by the loan originators once a certain repayment delay occurs (here: 60 days), including both the outstanding principal and accrued interest. So far, the buyback guarantee has been honored by all Esketit loan originators.

I’m Denny Neidhardt, the founder of re:think P2P. On this blog, I help retail investors make smarter, well-informed investment decisions in the world of P2P lending. Since 2019, I’ve been publishing in-depth analyses, platform reviews, and risk assessments to bring more transparency to this investment space. My goal is to challenge marketing claims, question developments, and empower investors with honest, independent insights.

Hi Denny, thanks for the review again!

You didn’t mentioned JMD Investments SIA in your list of lenders. Why is that?

Esketit has stopped publishing loans for Money for Finance (Jordan), but continues with JMD investments (Holding Jordan). Why is not really clear (regulation preparation?). Unfortunately, their communication is not anymore what it used to be.

Hi Thijs! Thanks for your comment.

On Friday, I started a bigger overhaul for the Esketit review which is not done yet. I expect this to be completed within the next few days. JMD Investments will then be included as well.

Have a good weekend,

Denny

After 5 months on Esketit I am at 6% IRR. WHY? Cashdrag. But not only. THe money will stay idle in your account for a week, then you will get a mini investment of a few euros, then again, nothing for days. Solution? Buy on the Secondary Market. I have counted in the last days up to 100.000 in loans, each day, put for sale with a Premium. So how come tens of thousand are issued daily and INSTANTLY put for sale? Well, Esketit will sell them to you with a premium. So buy as no other solution to stay invested. Hours later, or few days later it gets bought back. While this can happen, I don’t think it is a coincidence… 30% of what you buy on SM gets bought back in days… then probably reissued with a Premium. Not a transparent and honest platform.