Debitum Investments (formerly Debitum Network) is a P2P platform based in Latvia and regulated by the local financial supervisory authority. What makes Debitum special is its unique positioning in the P2P lending environment, as it is regulated, follows a marketplace model and offers buy-backed business loans. A combination that cannot be found in this form on any other P2P platform.

The innovations that have taken place since the change of ownership in August 2023 have significantly raised the profile and attractiveness of Debitum Investments. The improved loan supply, interest rates of up to 15% and the higher liquidity make Debitum one of the most exciting platforms to consider in 2024. At the same time, the new shareholders also have to deal with the legacy issues from the past, including the original ICO funding or the defaulted assets in Ukraine.

In this Debitum review, investors are given a detailed analysis of the platform and whether or not it is worthwhile to invest. Please note that all the information that are covered in this Debitum review are based on my own personal research and experiences. Make sure to do your own due diligence before investing on any platform.

Further analyses of other platforms can be found on my P2P Platform Review page.

Summary

Before we get started, here is a quick summary with the most important information about Debitum Investments.

- Debitum Investments is a Latvian P2P platform where investors can invest in buy-backed business loans from external lending companies, while earning a return of up to 15%.

- The platform is operated by SIA DN Operator, which has been controlled by the financial supervisory authority in Latvia since 2021 and is regulated in accordance with MiFID II. As a result, investors’ accounts are protected against misuse of funds or insolvency of the platform with up to EUR 20,000 by the investor compensation system.

- Since the change of ownership in August 2023, there have been a number of positive developments and new innovations on the platform. The loan supply, interest rates and liquidity have all been improved. New features such as Auto Invest have also been added.

- The platform has some legacy issues from the past. These include the crowdsale funding from 2017 (DEB Token) and the defaulted loans in Ukraine (Chain Finance).

| Founded / Started: | April 2019 / September 2018 |

| Legal Name: | SIA DN Operator (LINK) |

| Headquarter: | Riga, Latvia |

| Regulated: | Yes (Financial and Capital Market Commission) |

| CEO: | Anatoly Putna (October 2025) |

| Community Voting: | P2 out of 30 | See Voting |

| Assets Under Management: | EUR 60+ Million |

| Number of Investors: | 32.000+ |

| Expected Return: | 14.83% |

| Primary Loan Type: | Business Loans |

| Collateral: | Buyback Guarantee |

| Bonus: | 1% Cashback | 30 Days |

What is Debitum Investments?

Debitum Investments (formerly Debitum Network) is a Latvia-based P2P lending platform, launched in September 2018, where investors can fund business loans from SMEs and earn a return of up to 15%.

Debitum Investments (formerly Debitum Network) is a Latvia-based P2P lending platform, launched in September 2018, where investors can fund business loans from SMEs and earn a return of up to 15%.

The loans are not sourced by Debitum itself (with the exception of Sandbox Funding), but are offered from external lenders on the marketplace. Technically speaking, Debitum is therefore not a P2P, but a P2B (peer-to-business) platform.

The platform reached an important milestone in September 2021 when it was granted a licence as an investment brokerage firm. Since then, the platform has been supervised by the Latvian Financial Supervisory Authority and regulated in accordance with MiFID II.

The change of ownership in August 2023 is equally positive, as a result of which Debitum has seen a number of positive developments and new innovations. These include improvements for the loan supply, interest rates and liquidity. In addition, the Auto Invest function has also been reintroduced.

Fun fact: The Latvian word “Debitum” translates as “credit debt”.

The Origin Story

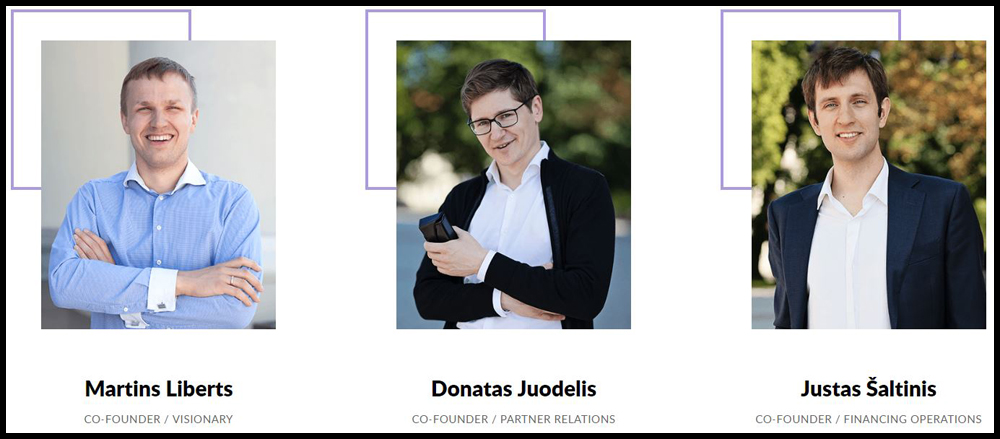

The idea of Debitum, then called Debitum Network, was born in 2017. The founders at the time included Martins Liberts, Donatas Juodelis and Justas Šaltinis.

Before founding Debitum, both Martins and Justas set up Lithuanian company DEBIFO. This was a lender specialising in invoice financing for small and medium-sized enterprises (SMEs) from Lithuania. The lender, which has also been financing some of its loans via Mintos, is now known as Factris.

Due to regulatory problems, DEBIFO had difficulties expanding its lending operations in other EU countries at the time. This problem initiated the idea of setting up a marketplace for similar lenders who faced the same issue. The idea of Debitum was born.

Following a token sale, which raised the equivalent of around EUR 6 million, the P2P platform was set up. The operational launch of the platform took place in September 2018.

Ownership and Management

Who are the main shareholders and management executives behind Debitum Investments? Let’s have a look!

Debitum Ownership

Who owns Debitum Investments? The Baltic-based P2P platform is operated by the company “SIA DN Operator”.

A look into the Latvian company register reveals that 100% of the shares belong to the company “ZIdea.” The beneficial owner of ZIdea is the Latvian citizen Ingus Salmins. Ingus has already been the majority shareholder of the P2P platform since July 2023. After his partner Eriks Rengitis sold his shares (approximately 33%) in October 2025, Ingus became the sole owner of the Debitum P2P platform.

Debitum Management

Operationally, since October 2025, Debitum has been led by the Latvian Anatoly Putna. He succeeds Debitum shareholder Eriks Rengitis, under whose leadership the platform was able to increase its managed portfolio from EUR 8 million to EUR 47 million.

Operationally, since October 2025, Debitum has been led by the Latvian Anatoly Putna. He succeeds Debitum shareholder Eriks Rengitis, under whose leadership the platform was able to increase its managed portfolio from EUR 8 million to EUR 47 million.

After studying economics at the Stockholm School of Economics in Riga, Anatoly initially worked as an investment specialist in the banking and finance sector. Following nearly three years at Crowdestor, he joined Debitum in May 2023, where he initially served as Chief Operating Officer (COO).

More information about the Debitum Investments team can be found on this page.

Business Model and Finances

Throughout the process of due diligence, investors should also have a look at the business model of a P2P platform as well as the overall financial situation. How does the company earn money? Does the platform operate profitably? And how well is the company positioned financially? In the following paragraphs of this Debitum review, you can follow-up on those questions.

Monetization

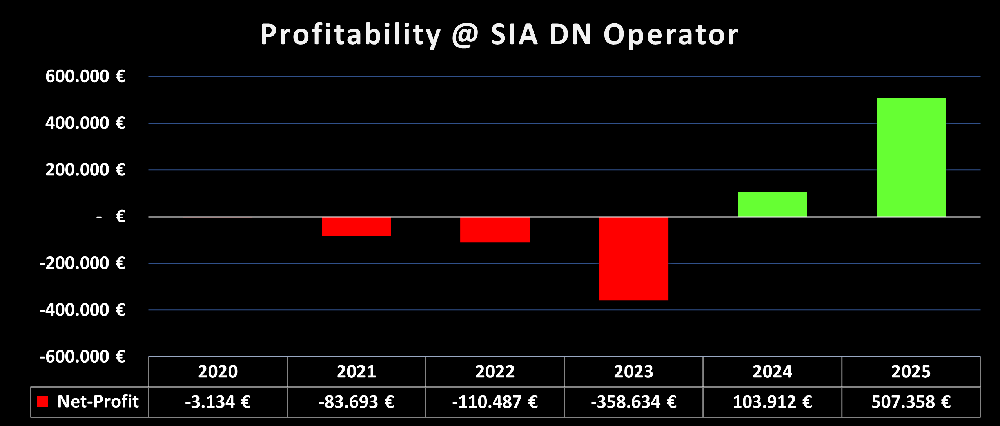

The P2P marketplace is primarily financed from commission income. These fees are charged to lenders for placing assets on the Debitum platform. As a result, Debitum was able to generate a revenue of EUR 2.4 million in the 2025 financial year. An additional EUR 20,000 was generated from other operating income.

Profitability

While revenue increased by 85% to EUR 2.4 million, operating expenses for marketing and salaries rose only slightly, by approximately EUR 436,000. As a result, Debitum was able to generate a profit of EUR 507,000 in 2025. The Latvian P2P marketplace has thus been profitable for the second consecutive year.

The 2025 financial report was prepared by the Latvian BDO Assurance and audited in accordance with IFRS standards. The figures therefore carry a certain level of credibility.

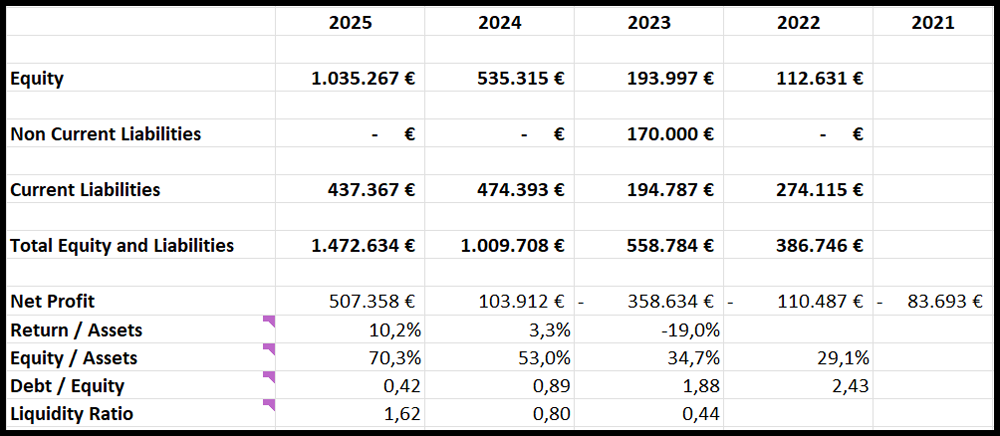

Balance Sheet

The balance sheet of SIA DN Operator has improved compared to the previous year.

The return on assets stands stands at a strong level of 10.2%, as does the equity ratio at 70.3%. In addition, the debt ratio (0.42) has been declining for the third consecutive year. The balance sheet is rounded out by a liquidity ratio of 1.62. Accordingly, there appears to be no issue regarding the P2P platform’s ability to meet its payment obligations.

Also positive: the company has recovered from accumulated past losses. At the end of the 2025 financial year, retained earnings amounted to EUR 55,267.

Overall, SIA DN Operator shows stable and healthy financial metrics, paving the way for a sustainable future growth of the P2P platform.

Sign Up and Bonus

In order to invest on Debitum, investors must meet two requirements: A minimum age of 18 years and a bank account in one’s own name. If these requirements are met, registration on Debitum can be completed in a few steps.

- Register: Enter name, email, date of birth, password, etc.

- Provide Financial Information: Planned investment amount, state citizenship, country of residence, tax residence, etc.

- Upload Documents: Copy of identity card, proof of residence

Also legal entities have the opportunity to register on Debitum.

Debitum Bonus

Investors who register on Debitum via this link will receive a 1% cashback on all investments made in the first 30 days after registration. Only assets with a term of 90+ days are taken into account.

A platform overview with all bonus offers and cashback promotions can be found on the bonus page.

Investing on Debitum

How does Debitum work and what should investors know and consider when investing on the plaform? In the following sections of my Debitum review you will find all the necessary information that you need.

Loan Offering

Debitum has been a regulated P2P platform, controlled by the Latvian financial regulator FCMC since 2021. Since this change happened, investors no longer invest in claim rights, but in asset-backed-securities (“notes”).

These are financial instruments that are composed of a bundle of different loans. The focus of Debitum is on business loans, which are offered by international lenders.

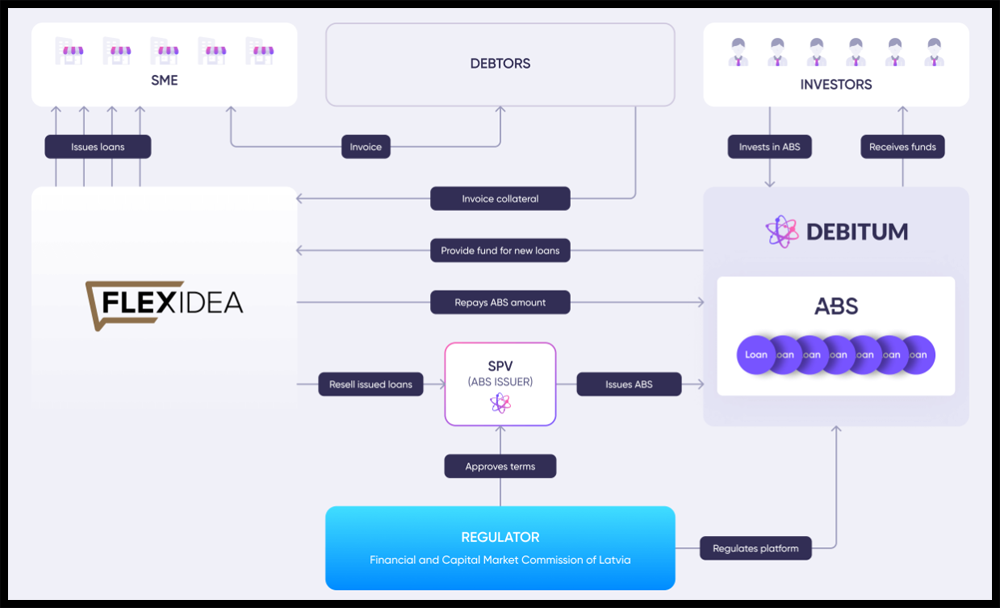

Debitum is very careful when assessing new lenders, which is why there are only a few long-term partners on the marketplace. These include Evergreen Capital (Estonia), Flexidea (Latvia and Poland) and Triple Dragon (UK). Other lenders include Sandbox Funding and Juno Finance (both Latvia).

- Sandbox Funding: Is owned by Debitum shareholders and was primarily founded to test lenders with smaller volumes before they appear independently on the platform. Currently the biggest lender on Debitum. More information in my Sandbox Funding article.

- Latvian Forest Development Fund: The Latvian fund, which joined Debitum in February 2025, is involved in the acquisition, management, and resale of Latvian forest land. More information in my Latvian Forest Development Fund article.

- Triple Dragon: The London-based lender offers flexible financing and working capital solutions for developers and publishers of mobile apps and video games. Receivables from companies such as Google, Apple and Amazon serve as collateral.

- Juno Finance: The Latvian lender, which has been on Debitum since April 2024, specialises in providing loans to SMEs in the forestry and agricultural sectors. Offers an interest rate of up to 15% and was previously tested with assets via sandbox funding.

- Foresto: Also based in the agricultural and forestry sector. A company founded in Latvia in 2021, which specialises in the purchase and merger and acquisition (M&A) of small and medium-sized forestry properties in Latvia. The collateralised notes (buyback after 20 business days) are offered with up to 12.5% and a maximum term of 12 months.

- Bono House: Subsidiary of the BONO Group (EUR 90M turnover in 2023), which was founded in Latvia in 2022. The lender specialises in the development of private house projects and the assembly construction in the real estate sector. The loans, which are collateralised with a buyback obligation, are offered with interest rates of up to 12% and terms of 90 to 250 days.

- Evergreen Capital: The Estonian lender, which has been on Debitum for many years, offers financing solutions for Estonian SMEs.

- Flexidea: Offers invoice financing solutions for Latvian and Polish SMEs. Long-standing partner of Debitum.

There is a fixed interest rate for the securities. This is amortised over the entire term as the underlying loans are repaid. The range on Debitum is between 8% and 15%. In some cases, it can also be up to 15%.

The minimum investment amount is EUR 50.

Debitum Notes (Bonds)

In addition to asset-backed securities (ABS), Debitum is offering notes (bonds) as a further investment product since March 2024. The difference to asset-backed securities is that the repurchase obligation no longer falls on the lender, but on the issuer’s shareholders.

In addition, payments are no longer linked to the underlying assets, but to the issuer as a legal entity. The first ten bonds were offered by Sandbox Funding, with a term of 6 to 12 months and an interest rate of between 13% and 13.5%.

Costs and Fees

There are no fees or hidden costs for private investors on Debitum. Neither for deposits or withdrawals, nor for the functionalities when investing on the platform.

Expected Returns

On Debitum, the expected return largely depends on the selection and performance of the respective loan originators. For example, Evergreen Capital often offers interest rates of only around 8%, while the Latvian Forest Development Fund can go up to 16.5%.

In addition, various bonus campaigns must be taken into account, which can further have a positive impact on return expectations.

Since my Debitum comeback in July 2024, I have been able to achieve a total return of 15.46%. Considering the risk profile of the platform, Debitum therefore offers one of the most competitive returns in the P2P lending space.

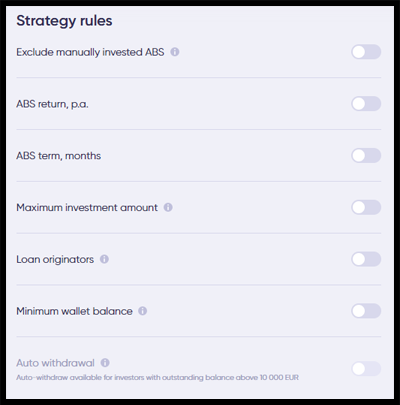

Auto Invest

In December 2023, Debitum has launched the long overdue Auto Invest feature, which is one of the common functionalities of a modern P2P platform.

Investors have the option of having their investments selected automatically based on previously set criteria. These criteria include the maximum portfolio size, the interest rate, the loan term or the selection of individual lenders.

The “Auto Withdrawal” setting is particularly interesting. Here, the monthly interest income is automatically transferred to the investor’s account. However, there is a restriction that only investors with an outstanding portfolio of EUR 10,000+ can use the Auto Withdrawal function.

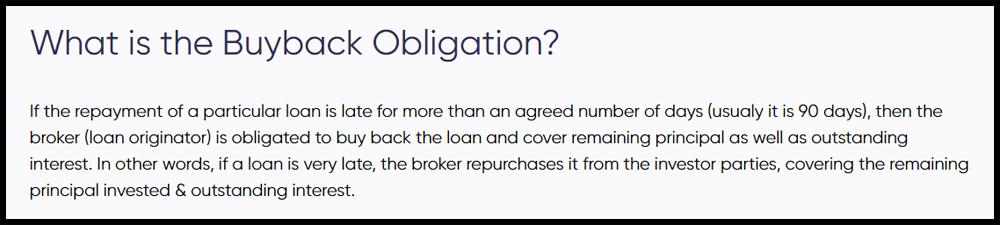

Buyback Guarantee

All assets offered on Debitum have a buyback guarantee issued by the lenders. This means that if the repayment of a particular loan is delay for an extended period of time (usually 90 days), the lender is obliged to buy it back and cover the remaining principal, as well as the outstanding interest.

In general, this buyback mechanism has always worked well. There is an exception with the Ukrainian lender Chain Finance though, where the repayment could not be met due to the war in Ukraine. Here, the platform invokes a force majeure.

Debitum Forum

The P2P lending industry is a fast-moving environment. Hence, make sure to stay on top of all relevant information by subscribing to my channels on Telegram or WhatsApp. This way, you will always receive the latest information from the P2P industry, including platform news regarding Debitum.

Debitum Taxes

In principle, interest income generated by loan financing is considered investment income and must be reported as such in the tax declaration. After obtaining the investment brokerage firm license in 2021, Debitum is now legally required to also withhold taxes on interest income that is collected through regulated financial instruments.

The applied tax rate is based on the country of tax residency and the tax information that are submitted.

- 20% for investors from Latvia

- 20% for investors outside the EU or EEA

- 5% for investors with residency in the EU or EEA (except Latvia)

- 0% for investors from Lithuania (tax certificate required)

- 0% for legal entities

When paying taxes in your county of residence, the withheld taxes can usually be deducted from the overall balance. This means that the effective taxation rate will be the same as it has been before when investing into claim rights. To get access to the relevant data, Debitum offers to download tax reports and income statements from the platform.

Debitum Risks

When considering a P2P platform, investors should take a very close look at the potential risk factors and evaluate them before making an investment. What should be considered in the specific case of Debitum? What are the underlying risks and how can they be assessed?

Platform Risk

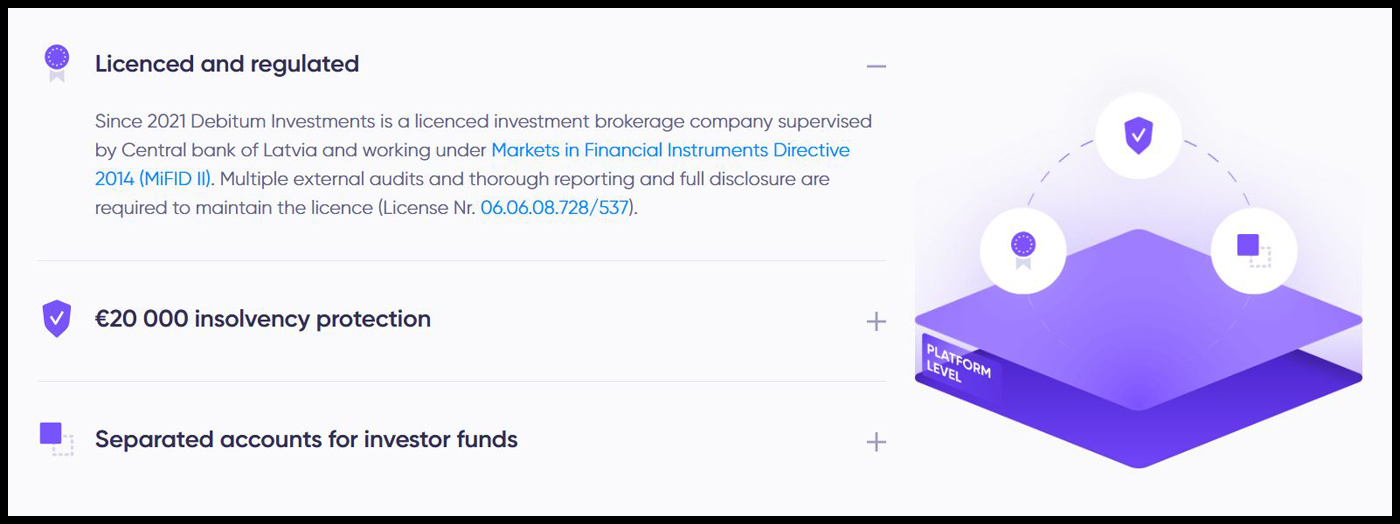

Debitum Investments, operated by SIA DN Operator, has held an investment brokerage license since September 2021, issued by the Latvian central bank. The platform is therefore subject to the requirements of the Markets in Financial Instruments Directive (MiFID II).

As a result, investors’ accounts are protected up to EUR 20,000 by the investor compensation system in Latvia in the event of the platform’s insolvency or misuse of investor funds. However, this does not cover potential defaults by the loan originators.

Due to the platform’s regulation, Debitum must also comply with a high level of compliance and transparency standards, which enhances the safety of the P2P lending platform.

Among other requirements, the platform must regularly prepare audited annual financial statements, allowing for an assessment of its financial stability.

In addition, investor funds must be kept separate from Debitum Investments’ own capital. In case of insolvency, these funds are not touchable by the bailiff and cannot be used to cover third party creditor claims.

Deposit Insurance

The investments offered through Debitum are not covered by European deposit guarantee schemes (such as the Deposit Guarantee Directive 2014/49/EU). This means that – unlike traditional bank deposits – funds invested on Debitum Investments are not insured or guaranteed by any national or European compensation scheme.

Accordingly, investors should be aware that the capital invested is subject to the risk of loss, that returns are not guaranteed, and that they may not recover the full amount originally invested.

ICO Scam Accusations

Debitum had to deal with scam accusations in the past. The background is a crowdsale funding (token generation event) from 2017, from which Debitum emerged. The accusation: Many investors felt deceived by Debitum in the promise to give the DEB token a meaningful use. Instead, it was only intended to provide funding for a business model primarily based on a FIAT currency.

The new Debitum shareholders, who took over the platform in August 2023 and who were not involved at the time, are disputing outstanding claims against the investors concerned.

Lender Risk

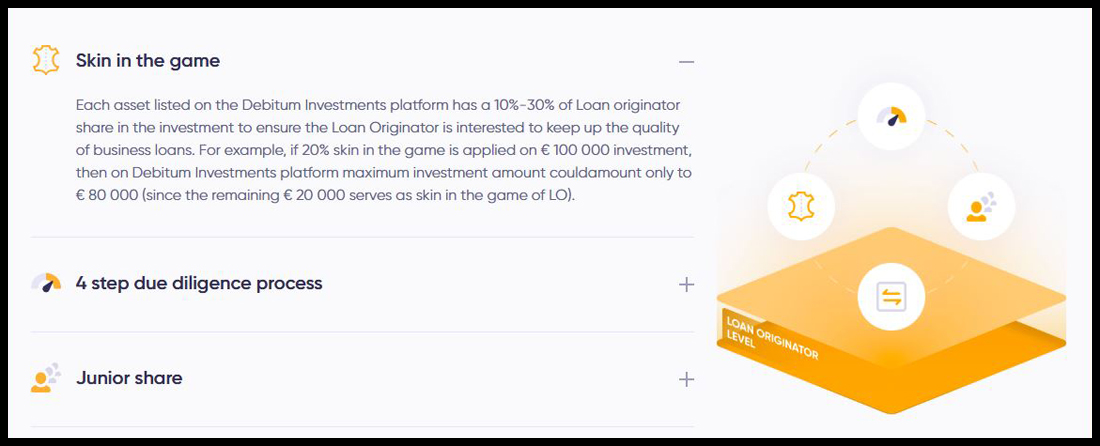

On Debitum, the lenders are required to finance between 10% to 30% of their loans with equity (skin in the game). This ensures that the lender has a vested interest in maintaining a good portfolio quality.

In the event of loan defaults, the lender is obligated to repurchase the loan within the specified timeframe (usually 90 days) as part of the buy-back obligation.

The ongoing fulfillment of the buyback guarantee depends largely on the lender’s risk management and financial situation. To allow for a better assessment, the following table provides an overview of all active lenders currently represented on Debitum. Check out the lender overview and comparison page for additional information regarding applied KPIs and their interpretation.

| Loan Originator | Year | Audited | Profit | ROA | Equity Ratio | Debt | Liquidity | Impairments | Score |

|---|---|---|---|---|---|---|---|---|---|

| Evergreen | 2024 | Unaudited | EUR 279K | 9,2% | 24,7% | 0,75 | 2,15 | 58 | |

| Juno | 2024 | Unaudited | EUR 158K | 1,4% | 7,6% | 0,92 | 0,99 | 38 | |

| LFDF | 2024 | S. Vilcānes Audits | EUR 70K | 1% | 15,9% | 0,84 | 1,19 | 48 | |

| Sandbox | 2024 | Latimira un Partneri | EUR 21K | 0,5% | 9,3% | 0,91 | 1,28 | 43 | |

| Terra Baltic | 2025 | S. Vilcānes Audits | EUR 265K | 91,9% | 98,9% | 0,01 | 84,02 | 65 | |

| Triple Dragon | 2024 | Unaudited | EUR 0 | 3,3 | 24 |

So far, all lenders currently active on Debitum have met their repayment obligations.

Chain Finance

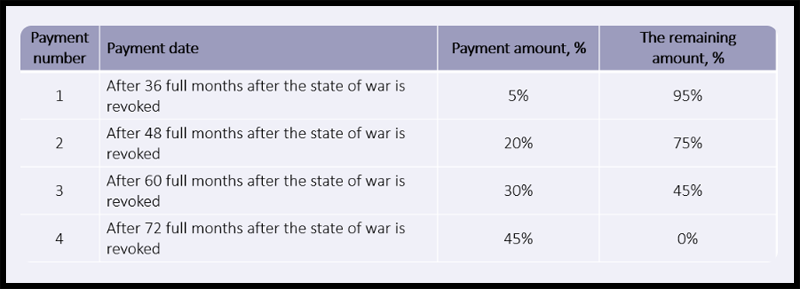

In the context of the outbreak of war in Ukraine, there was to date the only lender default on the Debitum platform. This involved the Ukrainian lender Chain Finance, which at the time of the default had approximately EUR 1.9 million in outstanding assets on Debitum. Repayment of the outstanding claims has been frozen indefinitely, citing force majeure.

In July 2023, the platform announced that a restructuring of the outstanding claims had taken place, in which the Debitum subsidiary “DN Funding Alpha” took over the obligations of Chain Finance towards Debitum investors. As part of this restructuring, Debitum has held out the prospect of full repayment of the loans affected by the war. Accordingly, the lender could repay the outstanding receivables six years after the end of the force majeure.

As a result, investor funds – which in theory could have been paid out immediately after the end of the war – would remain tied up for another four years. The fact that the former Debitum shareholders took this decision independently and without consulting with the affected investors, suggests a lack of investor interest by the platform.

The new Debitum shareholders favor a different approach by working toward an early settlement of the outstanding obligations. To achieve this, a buyer is to be found who will purchase the claims at a discount. This could result in a realized loss on the platform for the first time.

Advantages and Disadvantages

In this section, I have listed the biggest advantages and disadvantages of Debitum.

Advantages

- Regulation: The platform has held an Investment Brokerage Firm license since 2021.

- Track Record: Debitum has been active in the P2P lending space since 2018.

- Diversification: Diversification opportunities beyond traditional consumer loans.

- Expected Returns: Interest rates of up to 16%, in addition to bonus campaigns.

- Auto Invest: Automated option to invest in loans.

- Growth: Debitum is among the fastest-growing P2P platforms.

Disadvantages

- Ukraine: Debitum has independently extended the repayment period for Ukrainian loans.

Debitum Alternatives

Which Debitum alternative might be worth considering for investors? When focusing on business loans, one could think of the crowdfunding platform Crowdestor. Given a number of red flags, this platform might better be avoided. With regards to the marketplace model, alternatives such as Mintos (also regulated in Latvia) or Income Marketplace would come to mind. What exactly is there profile though?

Mintos

With EUR 600+ million in investor assets under management and more than 500,000 registered users, Mintos is the largest P2P lending platform in Europe. In addition to a wide range of loans, the Latvian P2P marketplace also offers other asset classes. These include ETFs, bonds or real estate. Additional information can be found in my Mintos review.

Income Marketplace

Income Marketplace is an unregulated P2P marketplace based in Estonia. The platform, which had its operational start in January 2021, markets itself with a range of innovative security features that are designed to provide investors with significantly better protection against problematic lenders. So far, investors have not suffered any losses on Income Marketplace yet. In addition, many of the lenders represented on Income offer an attractive combination of high interest rates and high liquidity. Further information on the Esketit alternative can be found in my Income Marketplace review.

You can find other Debitum alternatives on the P2P Platform Comparison page.

Community Feedback

Over the years, Debitum has established itself as one of the most popular alternatives in the P2P lending space. In the annual community voting, Debitum has consistently improved its ranking over the past three years. In 2025, it even secured second place among 30 participating P2P platforms.

Other P2P platforms in the top 5 included Viainvest, Mintos, Swaper, and Income Marketplace.

Summary Debitum Review

What is the final verdict of my Debitum review and my personal opinion?

What is the final verdict of my Debitum review and my personal opinion?

Debitum is one of the most exciting options in the P2P lending environment in 2024. The platform’s appeal derives from a mix of regulation, competitive interest rates and high liquidity.

This is in particular due to the change of ownership in August 2023, which has made Debitum significantly more agile and innovative.

In discussions with CEO and shareholder Eriks Rengitis, I was able to get a better idea about the expertise of the new owners. Due to his corporate finance background, Eriks may seem a little “dry”, but his experience and network from the M&A sector, coupled with his sharp mind, are useful advantages for the further development of the platform.

I therefore believe that Debitum is currently in good hands and has great potential to continue its current growth trajectory. As a consequence, I have decided to personally invest in Debitum again.

Debitum could be an attractive alternative for investors who prefer to invest their money in regulated P2P platforms and who want to diversify their loan portfolio aside from traditional consumer loans.

FAQ Debitum Review

Debitum (formerly Debitum Network) is a Latvia-based P2P lending platform, launched in September 2018, where investors can invest in SME business loans and earn returns of up to 16%. Since 2021, Debitum has been a regulated platform supervised by the Latvian Financial and Capital Market Commission (FCMC). Following this transition, investors no longer invest in assignment agreements (claim rights) but in loan-backed securities (“Asset-Backed Securities”). These are financial instruments composed of a bundle of different loans.

Both natural and legal persons can register on Debitum. To register as a natural person, investors must meet two requirements: a minimum age of 18 years and a bank account in their own name.

The interest rates on Debitum vary depending on the loan originator, ranging from 8% to 16%. Accordingly, the returns that investors can achieve may differ significantly. Since the change of ownership in summer 2023, interest rates on the platform have increased noticeably. My personal overall return has been around 14% since then.

The platform is operated by SIA DN Operator, which has been supervised by the Latvian financial regulator since 2021 and is regulated under MiFID II. This protects investor accounts up to €20,000 through the investor compensation scheme against misappropriation or insolvency of the platform itself. However, default risks at the loan originator level are not covered by this protection.

All assets offered on Debitum come with a buyback guarantee issued by the loan originators. This means that loans with a repayment delay (usually after 90 days) must be repurchased by the issuer. Both the remaining principal and any outstanding interest are covered under this guarantee.

I’m Denny Neidhardt, the founder of re:think P2P. On this blog, I help retail investors make smarter, well-informed investment decisions in the world of P2P lending. Since 2019, I’ve been publishing in-depth analyses, platform reviews, and risk assessments to bring more transparency to this investment space. My goal is to challenge marketing claims, question developments, and empower investors with honest, independent insights.

I have seen you have stopped with Debitum june last year.

I am considering to start with Debitum, as one of the few business loans platforms.

They are rated positively on other sites like p2plendingsites.com and p2pincome.com.

Can you specify the main reason(s) you stopped with Debitum?

It see quite a difference between your own IR results (in the end less than 6%, despite Debitum zero default rate), and what Debitum projects, 14%. That is my main concern. On paper things look good, but reality is quite different???

My biggest concern is that they don’t publicly share AUM development and the performance of their portfolio. Also, some of their data displayed is clearly misleading investors and the decision with regards to Chain Finance was clearly not made in favor of investors. Now they are pushing funds for new Sandbox lender that is owned by one of their founders and I don’t like this conflict of interest. I wouldn’t rule out an investment in the future again, but prior I want to see some improvements from their new owners.