A lack of transparency, pending payments, high risk. The narrative around Creditstar is relatively easy to summarize. But is it actually true?

Since June 2025, I have been actively invested in Monefit SmartSaver, a product from the Creditstar ecosystem. The offer strongly aligns with my personal investment strategy: maximum liquidity combined with the possibility to invest through my Estonian company.

In this article, I will explain how Monefit SmartSaver is currently positioned, how I personally use the product, which risks should be considered, and for whom an investment in the Estonian savings account alternative could be worthwhile.

Status Quo 2026

There are two ways to invest money via Monefit SmartSaver, operated by the Estonian company Monefit Card OÜ.

Main Account: 7.5% APY

The first option is the Main Account, where newly transferred funds are invested immediately and accrue interest on a daily basis. In June 2025, the effective annual yield (APY) on the Main Account was increased from 7.25% to 7.5%.

The first option is the Main Account, where newly transferred funds are invested immediately and accrue interest on a daily basis. In June 2025, the effective annual yield (APY) on the Main Account was increased from 7.25% to 7.5%.

The current minimum investment amount is EUR 10, which represents a low entry barrier for interested investors. On the other hand, the maximum investment amount is currently EUR 500,000.

SmartSaver Vault: Up to 10.52% APY

As an alternative to the Main Account, investors have been able to invest in “Vaults” since March 2024. This product is comparable to a fixed-term deposit.

Depending on the investment period, investors can achieve different levels of return.

- 6-month term: 8.33% APY

- 12-month term: 9.42% APY

- 18-month term: 9.96% APY

- 24-month term: 10.52% APY

The minimum investment amount for SmartSaver Vaults is currently EUR 100. The maximum investment amount is also EUR 500,000. Unlike the Main Account, the SmartSaver Vaults are particularly suitable for slightly longer-term investments where a higher return can be achieved.

More Planning Certainty and Liquidity

Monefit SmartSaver has introduced several new features in recent months aimed at improving liquidity and planning certainty for investors.

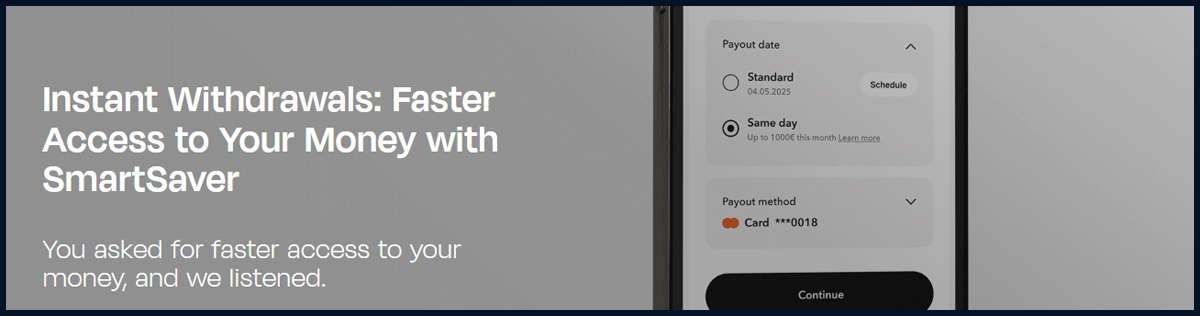

Since November 2025, investors have been able to withdraw up to EUR 1,000 per calendar month instantly from the SmartSaver Main Account. For amounts above EUR 1,000 per month, a processing time of up to 10 business days still applies. In addition, investors can now schedule their withdrawals up to 365 days in advance. Both one-time and recurring withdrawals can therefore be planned ahead.

Another feature was introduced in January 2026 under the name “Passive Income Mode.” This allows investors to automatically withdraw the interest accrued each month on the first day of the following month. However, this only includes returns generated through the Main Account. Bonus payments and earnings from the Vaults still need to be withdrawn separately.

Personal Use of Monefit SmartSaver

Since 2022, I have been running a business registered in Estonia. All revenues from my entrepreneurial activities are processed through this company.

Applying for the Estonian e-Residency program is relatively simple and straightforward, as is managing and handling the company’s accounting, thanks to qualified partners such as XOLO.

Beyond that, there are also some specific tax characteristics. In Estonia, retained or reinvested profits are subject to a 0% corporate tax rate. Instead, a tax of 22% is only applied at the company level when dividends are distributed to private individuals.

For this reason, I started to phase out my personal investor accounts on P2P platforms several years ago and instead registered again as a legal entity, allowing me to benefit as much as possible from the tax deferral effect.

For this reason, I started to phase out my personal investor accounts on P2P platforms several years ago and instead registered again as a legal entity, allowing me to benefit as much as possible from the tax deferral effect.

So far, I have made three larger dividend distributions from my company. This is exactly where Monefit SmartSaver comes into play. Instead of leaving my revenues on my Wise account, I use the Estonian liquidity product to temporarily park a part of the funds intended for those distributions.

Since my primary focus is liquidity rather than returns, I only use the Main Account on Monefit with its 7.5% yield and not the available Vault options.

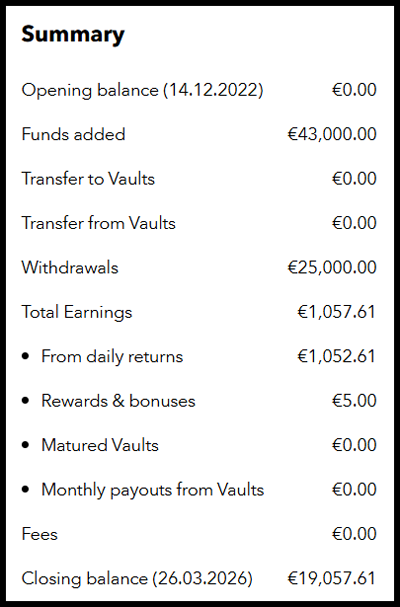

At times, I had more than EUR 30,000 invested in Monefit SmartSaver (December 2025). Currently, the account value is at around EUR 19,000. On March 12, 2026, I earned my first EUR 1,000 in interest through the platform. Not a bad result for just under 10 months.

Monefit SmartSaver Risks

The advantages of Monefit SmartSaver are also accompanied by several risks. What are they exactly, and how should they be assessed?

Platform Risk

In November 2022, the Monefit SmartSaver platform began its operations. The platform is operated by the Estonian company Monefit Card OÜ. In its domestic market in Estonia, the platform is not supervised by a financial or regulatory authority.

The price of this largely unrestricted operational freedom is therefore a lower level of oversight, regulatory control, and transparency.

Unlike traditional bank deposits, the funds invested on Monefit SmartSaver are not protected or guaranteed by a national or European deposit compensation scheme. As a result, the invested capital is subject to a risk of loss.

Lender Risk (Creditstar)

Monefit SmartSaver belongs to the Estonian Creditstar Group AS. The fintech company was founded in 2006 and includes a number of internationally active lenders across Europe.

Anyone who wants to understand how reliable the returns and liquidity on Monefit SmartSaver really are should take a closer look at both the past and present of the Creditstar Group.

Repayment Issues

At the end of 2024, Creditstar managed a gross loan portfolio of approximately EUR 414 million. Financing via P2P lending platforms is a frequently used component of the group’s overall funding strategy.

In the past, however, the Creditstar Group has not always been able to honour the promised buyback guarantees on time, for example on platforms such as Mintos or Lendermarket.

The reason for delayed repayments is that the Creditstar Group often follows an aggressive credit financing strategy. As a result, above-average default rates and volatility in the acquisition of external funding have repeatedly led to delays in repayments to investors.

This is likely also one of the reasons why Monefit SmartSaver was introduced as an additional and cost-efficient source of funding.

In the three-year history of the platform so far, all withdrawals have been processed within the stated timeframes. Nevertheless, investors should keep in mind that liquidity on Monefit SmartSaver may potentially be limited and cannot necessarily be guaranteed at all times.

Financial Stability

When looking at the present situation, it makes sense to take a closer look at the financial stability of the Creditstar Group AS.

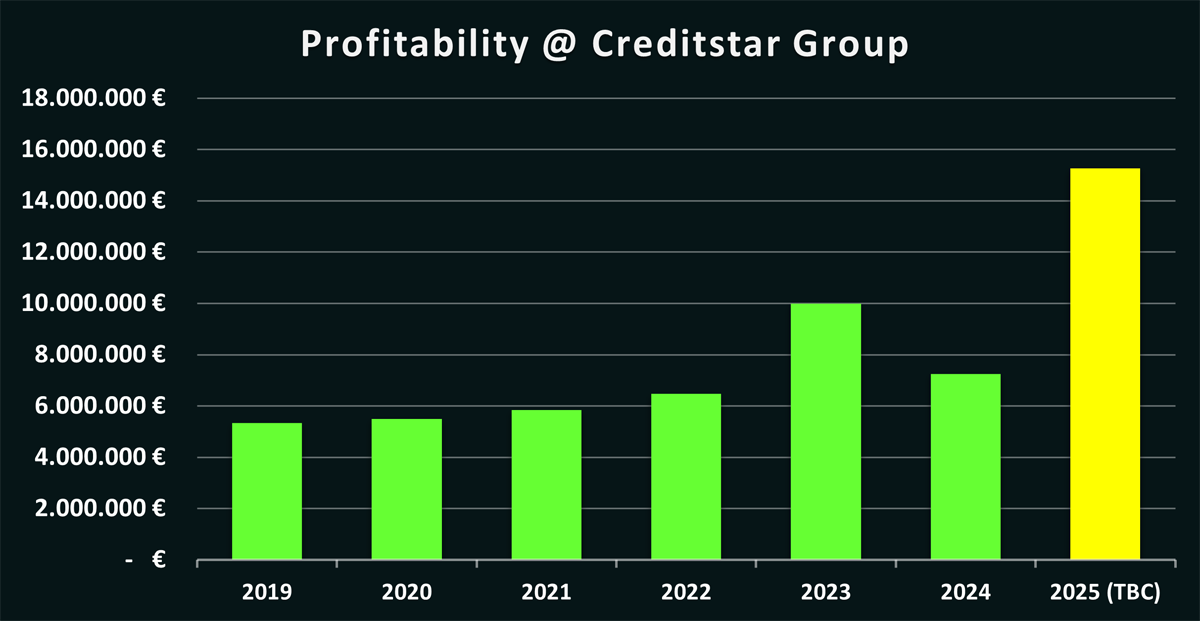

One positive aspect is that Creditstar has been publishing audited financial statements for many years, reviewed by KPMG and prepared in accordance with International Financial Reporting Standards (IFRS). As a result, the reported financial results can be considered credible.

The figures also show that the Creditstar Group has managed to build a profitable business model in the lending sector in recent years. Since 2019, the company has consistently generated profits in the mid-single-digit million range. According to the internal business development report, the group even achieved a profit of EUR 15.2 million in 2025, which would represent a doubling compared to the previous year.

Based on the criteria of my lender comparison, however, Creditstar achieved only average results in terms of return on total capital (2.2%), equity ratio (19.2%), and debt ratio (4.2).

Relatively weak results can be observed in metrics like the liquidity ratio (0.4) and the impairments ratio (15.2%). These figures also help to explain the repayment issues that have occasionally affected Creditstar’s reputation. Short-term assets and receivables are often matched by comparatively high short-term liabilities, while the quality of the loan portfolio still leaves considerable room for improvement.

| Loan Originator | Year | Audited | Profit | ROA | Equity Ratio | Debt | Liquidity | Impairments | Score |

|---|---|---|---|---|---|---|---|---|---|

| Creditstar Group | 2024 | KPMG | EUR 7,24M | 2,2% | 19,2% | 4,2 | 0,4 | 15,2% | 57 |

Overall, the Creditstar Group achieves a score of 57 points, which corresponds to a medium and average rating. On the lender page, the individual evaluation criteria are explained in detail, along with guidance on how to interpret the figures.

Loan Portfolio Transparency

Where exactly do the invested funds on Monefit SmartSaver go, and what performance do the underlying loans generate that ultimately fund the returns on the platform? This question has remained largely unanswered, as Monefit has not yet published detailed information about the performance of the underlying loan portfolio.

![]()

Although the platform now provides a statistics page that includes figures such as the number of investors, total invested volume, and average returns, important data points are still missing that would allow investors to better assess and evaluate the risk profile of Monefit SmartSaver.

Conclusion: Who Benefits from Monefit SmartSaver?

Monefit SmartSaver celebrated its three-year anniversary at the end of 2025. The results: more than 30,000 registered investors, EUR 18 million in interest paid out, and (perhaps most importantly) no withdrawal issues. Its establishment as a sustainable alternative to Bondora Go & Grow in the market is therefore hardly in dispute.

Monefit SmartSaver celebrated its three-year anniversary at the end of 2025. The results: more than 30,000 registered investors, EUR 18 million in interest paid out, and (perhaps most importantly) no withdrawal issues. Its establishment as a sustainable alternative to Bondora Go & Grow in the market is therefore hardly in dispute.

Key recent developments include the increase of the Main Account yield to 7.5%, longer-term options for the Vaults, and the ability to withdraw up to EUR 1,000 instantly per calendar month from their main account. For larger amounts, a 10-business-day processing time applies.

Monefit SmartSaver offers the greatest value to investors who place a high priority on liquidity and quick access to their funds. While liquidity may be limited in certain market phases, under normal circumstances SmartSaver is a solid option for parking funds short-term while earning a higher yield.

The yields offered by the SmartSaver Vaults, considering their longer terms and in comparison to other alternatives in the P2P market, are less competitive.

Monefit SmartSaver is therefore particularly suitable for income-oriented investors who require regular cash flows from their P2P investments. The recently introduced “Passive Income Mode” is a useful feature that allows investors to automate the withdrawal of their earnings.

It is currently not expected that Monefit SmartSaver will introduce new transparency standards in 2026 regarding portfolio size, use of funds, or loan performance. Investors should therefore carefully assess the Creditstar Group and the potential for limited liquidity.

Within my personal investment strategy, I plan to use Monefit SmartSaver for the liquidity-focused portion of my P2P portfolio.

I’m Denny Neidhardt, the founder of re:think P2P. On this blog, I help retail investors make smarter, well-informed investment decisions in the world of P2P lending. Since 2019, I’ve been publishing in-depth analyses, platform reviews, and risk assessments to bring more transparency to this investment space. My goal is to challenge marketing claims, question developments, and empower investors with honest, independent insights.